A plexiglass barrier between customers and tellers may be one of the few vestiges of the traditional banking experience that remain intact after all of this.

Amid ongoing concerns about the novel coronavirus and anticipation of a second wave of infections, age-old industries are rethinking daily operations. Retail and Hospitality is no exception and it has a new buzzword: contactless.

Contactless transactions are ubiquitous in many parts of the world. Americans, however, have been slow to adopt them. In the U.S., the highly anticipated “death of the wallet” simply never materialized. In 2018, just 3% of cards in use in the U.S. were contactless, versus around 64% in the U.K. and up to 96% in South Korea, according to a study by global management consulting firm A.T. Kearney.

But as Americans slowly emerge from their coronavirus-induced quarantines, blinking in the sunlight and wondering what, exactly, this “new normal” has in store for them, contactless payments begin to make a whole lot more sense.

What Are Contactless Payments, Anyway?

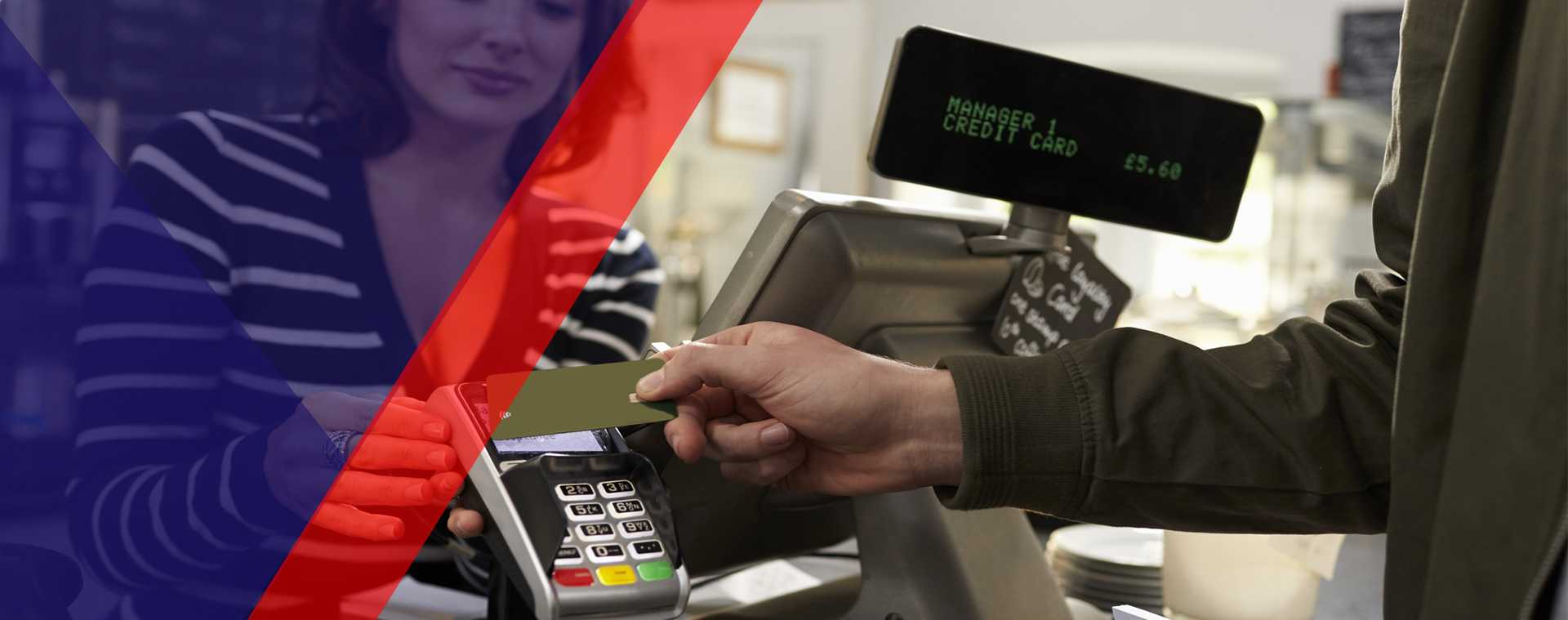

Contactless payments are pretty much what they sound like—a way of paying for goods or services without physically needing to swipe your card in a machine or pass it to another person. If you have even seen a passerby tap their phone at a checkout counter to pay for their latte, you have witnessed the technology in action.

As customers increasingly demand expediency—and now, assurances that store clerks and bank tellers will stay physically distant—more brick-and-mortar businesses are turning to Contactless solutions that do not require the consumer to touch or sign or have any physical contact or exchange of their payment cards with clerks or cashiers waiters or waitresses in the hospitality segment.

Banks and card issuers may be smart to ride the tailwinds created by COVID-19 and capitalize on the trend. Overall usage of contactless payments in the country has risen 150% since March 2019. But even before the pandemic, banks were implicitly nudging customers toward contactless payments by offering rewards for using platforms like the recently launched Apple Card.

How Contactless Payments Work?

Typically, the contactless payment systems work by utilizing radio-frequency identification (RFID), a widespread technology built upon electromagnetic fields. RFID employs memory chips that store data or “tags,” plus RFID readers that decode the message. Using this technology, physical objects in close proximity can talk to one another. These systems are used for everyday tasks like package-tracking, inventory management and toll collection.

Contactless payment systems often rely on near-field communication (NFC). This is a newer and more complex technology that falls under the RFID umbrella. Unlike RFID, which functions at many feet, NFC only works when there is a small distance between objects—usually a few centimeters. So, there is no danger that you will accidentally pay for a stranger’s groceries if you pass them in the checkout line.

The NFC Reader

NFC is the underpinning technology for services like Apple Pay and Google Pay. Cardholders enrolled in these services can use contactless payment platforms on their smartphones, watches, or other wearable devices for fast and easy transactions at point-of-sale (POS) terminals. All Biz Systems offers an NFC reader for businesses looking to jump on the mobile and contactless bandwagon.

NFC technology enables a variety of everyday activities beyond payments, too. It is used for e-ticketing, for instance. Users can tap a transit card or smart device to enter a subway turnstile or hop on a bus. New York City’s Metropolitan Transportation Authority (MTA) is currently rolling out OMNY, a contactless way to pay for public transit around town. If all goes to plan, the system will replace the MetroCard by 2023.

In the context of banking, cardless ATMs allow customers to withdraw money with a simple swipe, scan or tap. Instead of physically inserting a debit card into the machine, these ATMs let customers withdraw cash via smartphone app.

Some banks have proprietary apps for accessing cardless ATMs, while others work with third-party mobile wallets like Apple Pay. These apps generate verification codes (a QR code, for instance) or display a digital version of the user’s debit card. Users scan the code or tap the device near an indicated spot in the ATM booth, and voila—transaction complete.

Some ATMs also have NFC-enabled capabilities that let users tap their debit cards in an indicated area on the machine instead of manually typing in a personal identification number (PIN) on a keypad.

Both NFC-enabled and EMV debit cards contain chips, so a “chip card” can refer to either. Only NFC-enabled cards, however, will function for no-touch payments and cardless ATM transactions. Cardholders can easily tell if their card has NFC capabilities by checking for the contactless indicator, which looks like a Wi-Fi symbol turned sideways.

Benefits and Considerations for Contactless Payments:

Specific to transaction limitations, countries around the globe are reassessing these limits, as the need for contactless payments becomes more pressing in the wake of COVID-19. NFCW.com, an online portal that provides news and analysis specific to emerging payment technologies, reports in its May 28 update that 49 countries have announced contactless payment transaction limit increases, ranging from 25% to 400%, with an average of 131%.

For added peace of mind, cardholders can check with payments providers to see what specific steps ensure data security—many dedicated FAQ sections exist to address customer inquiries about the safety of contactless payments. Visa addresses the technology behind this method of payment on its site, and Apple Pay offers a lengthy explainer on its support forum about how it employs data encryption.

Contactless payments are a convenient way for customers, retailers, and banks to conduct seamless, swift, and socially distant transactions. Once set up, the systems are relatively maintenance-free. There are several possible downsides to contactless payments, however. Below are a few considerations:

Antiquated systems that do not accept contactless payments. If retailers or bank branches do not have updated POS terminals installed at checkout or an ATM, you will have to go old-school with an EMV chip dip or traditional swipe.

Paying for Stuff in a Post-COVID World

In early March, the World Health Organization warned that banknotes may be capable of carrying and spreading the novel coronavirus. Although the jury is still out on just how likely it is to catch COVID-19 by touching surfaces or objects, brick-and-mortar businesses and bank branches are likely to want to minimize the risk of infecting customers, however minuscule it may be.

On its banking blog, Accenture listed “a strong push toward a cashless society” as the No. 1 potential long-term impact that the pandemic may have on global payments processes. MasterCard polled 17,000 consumers in 19 countries and found that they perceive contactless payments as “the cleaner way to pay.”

If these predictions and sentiments manifest, bank customers can expect a quite different transaction experience going forward. For one thing, they may spend less time waiting in lines, as contactless payments lend themselves to speedier transactions. While the transaction time for a chip-enabled card can be as much as 30 to 45 seconds, a contactless transaction can reduce that to as little as 10 to 15 seconds.

From tap-to-pay debit transactions to no-touch ways to pay for public transit, the current landscape is fertile ground for contactless technology to take off.